Disclaimer

As the country moves through 2026, the UK economy stands at a pivotal juncture, caught between modest growth, persistent price pressures, and the lingering effects of global instability. Incomes, jobs, prices and policy decisions are all in flux, leaving households, businesses and policymakers to navigate a complex economic landscape.

This article breaks down the latest official data, forecasts and expert analysis, explains what the numbers mean for real people, and explores the likely economic path for the rest of the year.

Subdued Growth Despite Resilience

One of the first major indicators of the UK’s economic health is gross domestic product (GDP), which measures the total value of goods and services produced across the country.

According to the Office for National Statistics most recent data, the UK economy expanded by just 0.1% in the final quarter of 2025, reflecting a pattern of subdued growth rather than robust expansion. The slight increase was seen as a sign that the recovery has been hesitant and uneven across sectors.

Analysts interpret these numbers as confirmation that the UK’s recovery is still fragile. While output is positive overall, it is far below the pace needed to rapidly boost living standards or significantly reduce unemployment.

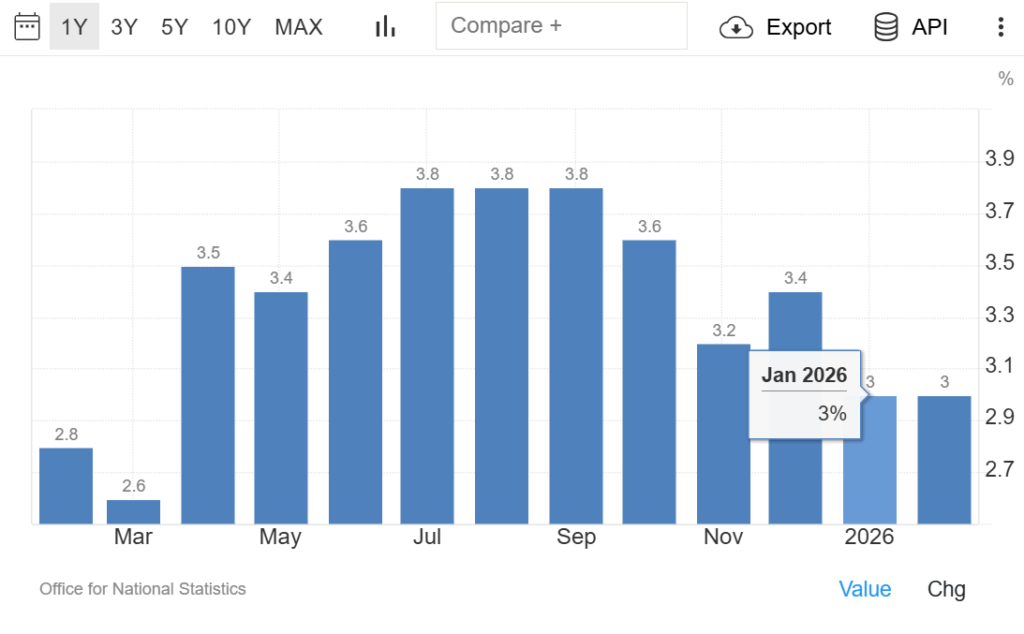

Inflation: Above Target but Not Sky‑High

Inflation is another core measure tracking the cost pressures facing households and businesses. The Bank of England aims for inflation around 2%, but the most recent Office for National Statistics figures show that UK consumer price inflation held at 3.0% in February 2026. This matched January’s rate, but policymakers and economists warn this figure could rise again due to external pressures, particularly surging energy costs linked to global conflict and supply bottlenecks.

Inflation has been driven in part by global energy price increases and cost pressures in services and goods. A Citi survey of public expectations saw anticipated inflation jump sharply, a rare spike in long‑term expectations that can make households feel the financial squeeze more acutely.

While inflation has eased from peaks seen in prior years, these figures remain above the Bank of England’s long‑term target, which continues to shape monetary policy decisions.

Source: tradingeconomics.com

Monetary Policy: Caution Over Cuts or Hikes

Against this backdrop, the Bank of England has taken a cautious stance on interest rates. In late 2025, the Bank’s Monetary Policy Committee chose to maintain Bank Rate at 4%, a level set to balance inflation and growth risks.

Most recently, Bank of England policymaker Alan Taylor emphasized the importance of holding rates steady amid uncertainty from global events. Taylor argued that while inflation pressures remain real, the economy’s response to recent shocks, including rising energy prices and softening demand, warrants caution before cutting or raising rates.

Such decisions are significant: higher interest rates make borrowing more costly for households and businesses, while rate cuts could spark wage and price pressures if inflation rebounds.

Labour Market: Mixed Signals

The UK labour market shows a nuanced picture. Unemployment levels have ticked higher compared to the recent past, raising concerns about weakening job demand. According to official sources, the unemployment rate was roughly 5.2% at the end of 2025, one of the higher figures seen in recent years.

Labour market data is particularly important because it affects consumer spending and confidence. When jobs are plentiful, people spend more; when they feel insecure, they rein in purchases and build savings, a trend reflected in recent consumer sentiment surveys showing lower confidence.

Consumer Confidence Sinks Amid Global Pressures

In March 2026, consumer confidence in the UK fell to its lowest level in 11 months, according to GfK’s long‑running confidence index. The decline was driven primarily by geopolitical concerns linked to the war in the Middle East and rising energy costs, which in turn have affected public expectations about economic stability and future household finances.

Rising oil prices, which have climbed significantly in recent months, have contributed to increased petrol pump prices and concerns that energy bills could rise further, especially after caps on tariffs are due to expire later in the year.

This combination of price pressures, geopolitical risk and slipping confidence paints a picture of cautious consumers who may delay major purchases, further slowing growth.

Growth Forecasts: Slightly Weaker but Not Stagnant

Multiple economic forecasts now point to modest growth in 2026, slower than previous expectations but consistent with a cautious recovery narrative.

The Office for Budget Responsibility’s March 2026 outlook projects that UK GDP will grow by around 1.1% in 2026, with inflation returning toward target levels and unemployment gradually easing later in the forecast period.

Independent forecasts paint a similar picture. The Bank of Ireland’s UK Outlook report anticipates around 1.0% growth in 2026, with unemployment rising to about 5.5% before easing in subsequent years.

Analysts have underscored that growth is likely to remain moderate rather than strong, reflecting ongoing headwinds from global uncertainty, tighter fiscal policy, and a cautious business environment.

Cost of Living and Real Wages

One of the most enduring economic stories in recent years, the UK cost‑of‑living crisis, continues to influence how households perceive economic conditions. The crisis is broadly characterised by rising costs for essentials like energy and food outpacing wage growth and putting pressure on household budgets.

While headline inflation has eased from its peaks, real wage growth (wages adjusted for inflation) remains compressed for many households. This dynamic can reduce discretionary spending, contributing to slower consumer demand and adding pressure on the broader economy.

Financial Markets and Business Conditions

The UK’s financial markets have reflected these broader economic uncertainties, with UK stock indices like the FTSE 100 losing ground this year amid rising energy prices and inflation concerns. Bond yields have also risen, increasing borrowing costs for both public and private sectors.

Business confidence has shown mixed signals, with some surveys suggesting stronger activity in parts of the services sector even as cost pressures build. These nuanced trends suggest that certain industries may be more resilient than others.

Read More: What Is Inflation and How It Affects Your Money in 2026

Policy Responses: Government Forecasts and Budgets

In early 2026, Chancellor Rachel Reeves delivered the Spring Statement, a key fiscal policy update for the UK. While the statement did not include major tax changes, it confirmed existing pension, benefits and savings policies and sought to reassure markets that the government’s economic plan was on track.

The OBR’s long‑term forecast also suggests fiscal sustainability challenges, including high public debt as a share of GDP, an issue that shapes government spending and taxation decisions for years to come.

Regional Disparities and Long‑Term Structural Trends

London and the South East continue to generate higher economic output than other regions, while some parts of the UK show slower expansion and investment, a pattern that reflects longstanding regional disparities and influences local labour markets and incomes.

Meanwhile, long‑term structural trends, including productivity challenges and the adoption of new technologies such as AI, will shape the UK’s future competitiveness. Some research suggests that increased investment in digital and green technologies could enhance productivity and growth over the next decade.

Read More: U.S. Insolvent? Treasury Financials Reveal Massive Liabilities Experts Say

A Fragile but Persistent Recovery

The UK’s economic outlook for 2026 is one of fragile recovery, persistent inflation above target, modest growth forecasts and cautious monetary policy. Household costs remain a central concern, while labour market dynamics and consumer confidence will be critical in determining the broader trajectory.

For policymakers, balancing inflation control with growth support remains a central challenge. For households and businesses, the year ahead will likely involve careful budgeting, cautious investment decisions, and close attention to global developments that influence energy and price trends.

This analytical story combines the latest data and expert forecasts with on‑the‑ground implications, making it useful not just today but for readers returning to the UK economy in the months and years ahead.

For more finance reporting and in-depth analysis, visit the Finance section at bdesk.news.

Ethan R. Brooks is a journalist with over 11 years of experience, specializing in finance, politics, and breaking news. He delivers timely, accurate reporting on market trends, economic developments, and major political events, helping readers stay informed on the stories that matter most.